18 Jun CP204 Instalment Changes Malaysia — YA 2027 Transitional Rule and YA 2028 New Schedule Under Finance Act 2025

CP204 Instalment Changes Under Finance Act 2025 — What Companies Must Know for YA 2027 and YA 2028

The Finance Act 2025, gazetted on 31 December 2025, restructures the CP204 tax instalment payment schedule for companies and limited liability partnerships in Malaysia. The changes take effect across two years of assessment — a transitional year in YA 2027 and a permanent structural change from YA 2028 onwards. Both are now enacted law. Companies and their tax advisers need to act on both.

The Problem the Change Solves

Under the current practice, a company’s 12 monthly CP204 instalments begin in Month 2 of its basis period and end in Month 1 of the following year. This means the final instalment for any given year of assessment spills into the next calendar year — creating a cross-year mismatch between when instalments are paid and when the underlying tax liability falls.

The Finance Act 2025 amendment eliminates this spill by aligning all instalment payments within the same basis period as the tax liability itself.

Three-Phase Comparison

| Aspect | Current Practice (Pre-YA 2027) | YA 2027 (Transitional) | YA 2028 Onwards (Permanent) |

|---|---|---|---|

| First instalment | Month 2 of basis period | Month 2 of basis period | Month 1 of basis period |

| Number of instalments | 12 | 11 only | 12 |

| Final instalment | Month 1 of next YA | Within same YA | Within same YA |

| Cross-year spill | Yes | No | No |

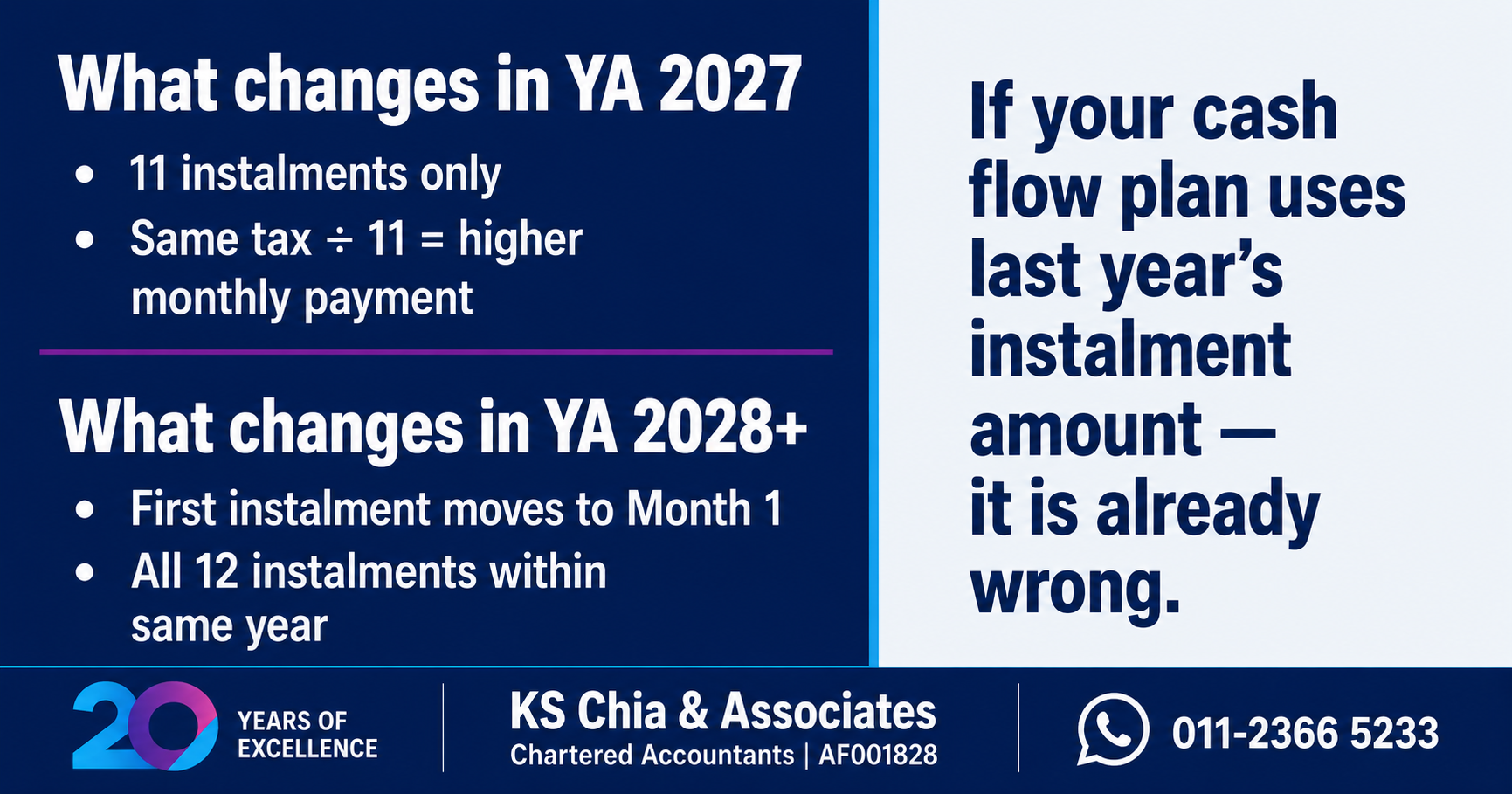

YA 2027 — The Transitional Year

For companies whose basis period falls in YA 2027, the instalment schedule works as follows:

- Instalments begin from Month 2 of the basis period — no change to the start month

- To ensure all instalments complete within YA 2027, the total number of instalments is capped at 11 months

- The total tax payable is unchanged — it is simply divided across 11 instalments rather than 12

- Each monthly instalment is therefore slightly higher than in prior years

The e-CP204 system for YA 2027 is now open for submission.

Cash flow implication: a company that budgets monthly tax instalment payments based on the prior year’s amount will be underfunded. The per-instalment amount must be recalculated using the YA 2027 estimated tax divided by 11, not 12.

YA 2028 Onwards — Permanent New Rule

From YA 2028, the full structural change takes effect:

- The first instalment moves to Month 1 of the basis period — one month earlier than current practice

- A full 12 instalments are payable, all completing within the same basis period

- No cross-year spill from YA 2028 onwards

Worked example — December year-end company (basis period 1 January 2028 to 31 December 2028, YA 2028):

- The CP204 submission deadline remains governed by Section 107C(2) of the ITA 1967 — not later than 30 days before the basis period begins. For a basis period starting 1 January 2028, this means CP204 must be submitted by approximately 2 December 2027.

- The first instalment payment for YA 2028 falls in Month 1 of the basis period — January 2028 — one month earlier than the Month 2 start under the current rule.

These are two separate dates and should not be confused: the CP204 form must be filed by early December 2027, while the first monthly instalment payment itself is due the following month, in January 2028.

What Does Not Change

- The CP204 submission deadline rule under Section 107C(2) — not later than 30 days before the basis period begins — is unaffected by this restructuring. Only the instalment start month and count are changing, not the filing deadline itself.

- CP204A revisions remain available at the 6th, 9th, and 11th months of the basis period.

- The 10% penalty on each unpaid instalment remains in force

- The 10% penalty on underestimation where the estimate falls short of actual tax by more than 30% remains unchanged

The Audit Planning Benefit from YA 2028

From YA 2028, CP204 instalment payments and the financial year will be fully aligned for the first time. All 12 instalments will fall within the same basis period as the tax liability they relate to. This eliminates the cross-period adjustments that currently arise at year-end when the final instalment spans two financial years, simplifying both the tax computation and the audit of the tax provision.

Action Points

- YA 2027 (immediate): Confirm that the YA 2027 CP204 has been recalculated using 11 instalments. Monthly cash flow budgets should reflect the higher per-instalment amount.

- YA 2028 (planning now): Confirm both your CP204 submission deadline (30 days before your basis period begins) and your first instalment payment date (Month 1 of the basis period) separately — they are not the same date.

- CP204A revisions: The 6th, 9th, and 11th month revision windows remain available. Use them if the tax estimate requires adjustment during the year.

Need Help?

If your YA 2027 CP204 has not been recalculated, or you are unsure of your exact CP204 submission deadline or first instalment date under the new YA 2028 rules, contact us. You may also want to check whether your CP204 has been filed and your tax fee is deductible — a separate but related compliance check every company director should run.

For broader support on corporate tax compliance, see our tax consultancy services.

KS Chia & Associates Chartered Accountants (AF001828)

WhatsApp or call:

011-2366 5233

Based on: Finance Act 2025 (gazetted 31/12/2025);

Section 107C, Income Tax Act 1967.