14 Jun Is Your CP204 Filed and Your Tax Fee Deductible? Two Checks for Malaysian Company Directors

Two compliance points that affect every Malaysian company with a tax filing obligation — and that are more commonly missed than most directors realise. The first concerns a statutory filing that carries criminal penalties if missed. The second concerns the deductibility of professional fees that many companies claim without meeting the conditions that make the deduction valid.

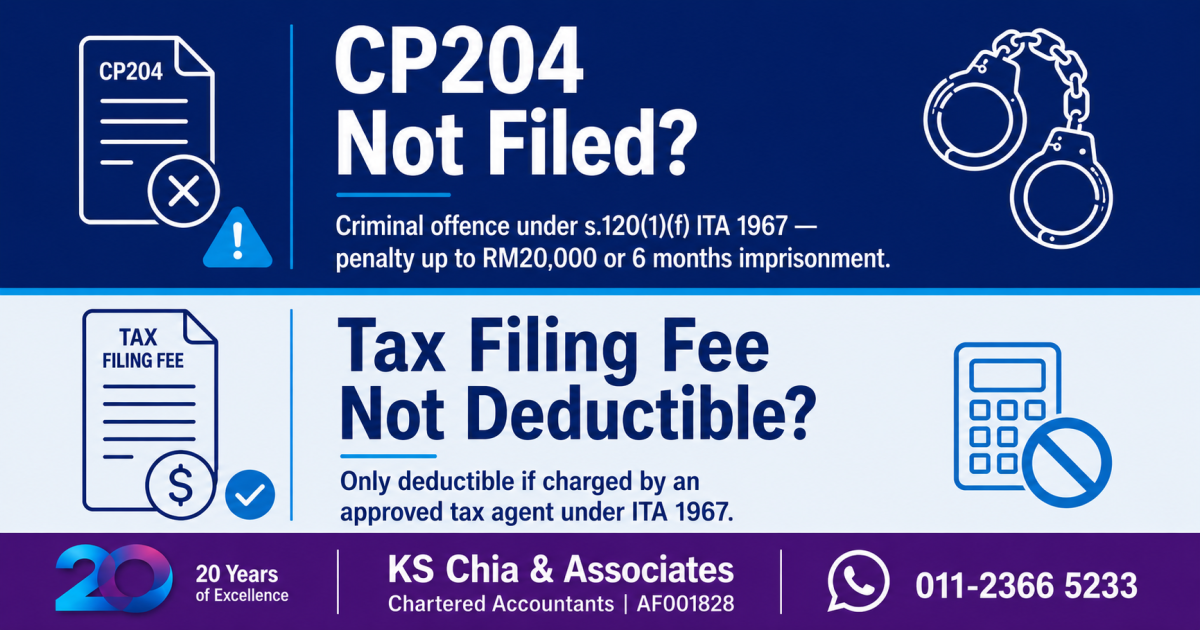

Point 1 — Failure to File CP204 Is a Criminal Offence

Form CP204 is the company’s estimate of tax payable for a year of assessment, required under Section 107C of the Income Tax Act 1967 (ITA 1967). It must be submitted by the 30th day of the second month of the basis period for the relevant year of assessment. This is a separate statutory obligation from the actual payment of tax instalments.

Failure to submit CP204 — whether missed entirely or submitted outside the prescribed deadline — is a criminal offence under Section 120(1)(f) of the ITA 1967. The statutory consequences are:

- A fine of between RM200 and RM20,000

- Imprisonment of up to six months

- Or both

This is not a late payment surcharge or a civil penalty. It is a criminal offence provision. LHDN treats the non-submission of CP204 as a compliance breach separate from any question of whether tax is ultimately owed.

Directors should confirm with their tax agent that CP204 has been submitted for the current year of assessment, and that a filing record exists. A verbal confirmation is not sufficient — request evidence of submission.

Point 2 — Tax Filing Fees Are Only Deductible If Your Provider Is an Approved Tax Agent

Under LHDN Guideline LHDN.AG.600-1/7/3 (updated 10 November 2023) and the Income Tax (Deduction for Expenses in Relation to Secretarial Fee and Tax Filing Fee) (Amendment) Rules 2021 [P.U.(A) 471/2021], fees for the preparation and submission of the following are deductible as a business expense:

- Income tax returns under Sections 77, 77A, 77B, 83, and 86 of the ITA 1967

- CP204, CP204A, and CP204B under Section 107C of the ITA 1967

- Sales tax and service tax returns under the Sales Tax Act 2018 and Service Tax Act 2018

The combined deduction for secretarial fees and tax filing fees is capped at RM15,000 per year of assessment from YA 2022 onwards. From YA 2022, the deduction is allowed once the expense is incurred in the basis period, even if payment has not yet been made.

The condition that is most frequently overlooked: the fee must be charged by an approved tax agent under the ITA 1967. A general

accounting firm, bookkeeping service, or management company that is not registered as an approved tax agent under the ITA 1967 does not meet this requirement — regardless of how the invoice is described or what services were performed.

Two additional points from the guideline:

- Disbursements and out-of-pocket expenses — telephone, postage, printing, travel — are expressly excluded from the deduction even when bundled into the total fee

- Secretarial fees are only deductible when paid to a company secretary registered under the Companies Act 2016 (Akta 777)

The Practical Implication

A company paying tax preparation and filing fees to a provider who is not an approved tax agent is bearing a business cost that generates no tax relief. At a corporate tax rate of 24%, a RM10,000 tax filing fee paid to a qualified approved tax agent carries a net cost of RM7,600 after the deduction. The same fee paid to an unapproved provider costs RM10,000 net — with no relief and no valid deduction to claim.

The description on the invoice does not change this. An invoice from an unapproved provider described as “tax advisory fee”, “accounting fee”, or “professional fee” does not become deductible by virtue of its label. The qualifying condition is the status of the service provider, not the wording of the invoice.

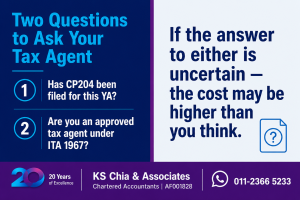

Two Questions to Check Before Your Next Filing Cycle

- Has CP204 been submitted for the current year of assessment — and is there a submission record to confirm it?

- Is the provider charging for your tax filing services an approved tax agent registered under the Income Tax Act 1967?

If either answer is uncertain, it is worth resolving before LHDN raises the question.

Need Help?

KS Chia & Associates Chartered Accountants is an approved tax agent under the Income Tax Act 1967 and a licensed audit firm. If you need to review your current compliance position or confirm your fee deductibility, contact us.

KS Chia & Associates Chartered Accountants (AF001828)

WhatsApp us at 011-2366 5233

Regulatory references: Section 107C and Section 120(1)(f), Income Tax Act 1967; LHDN Guideline LHDN.AG.600-1/7/3 (10 November 2023); Income Tax (Deduction for Expenses in Relation to Secretarial Fee and Tax Filing Fee) (Amendment) Rules 2021 [P.U.(A) 471/2021].