14 Jun e-Invoice and the Means Test: What Company Directors in Malaysia Must Know in 2026

The Means Test Has a New Data Layer

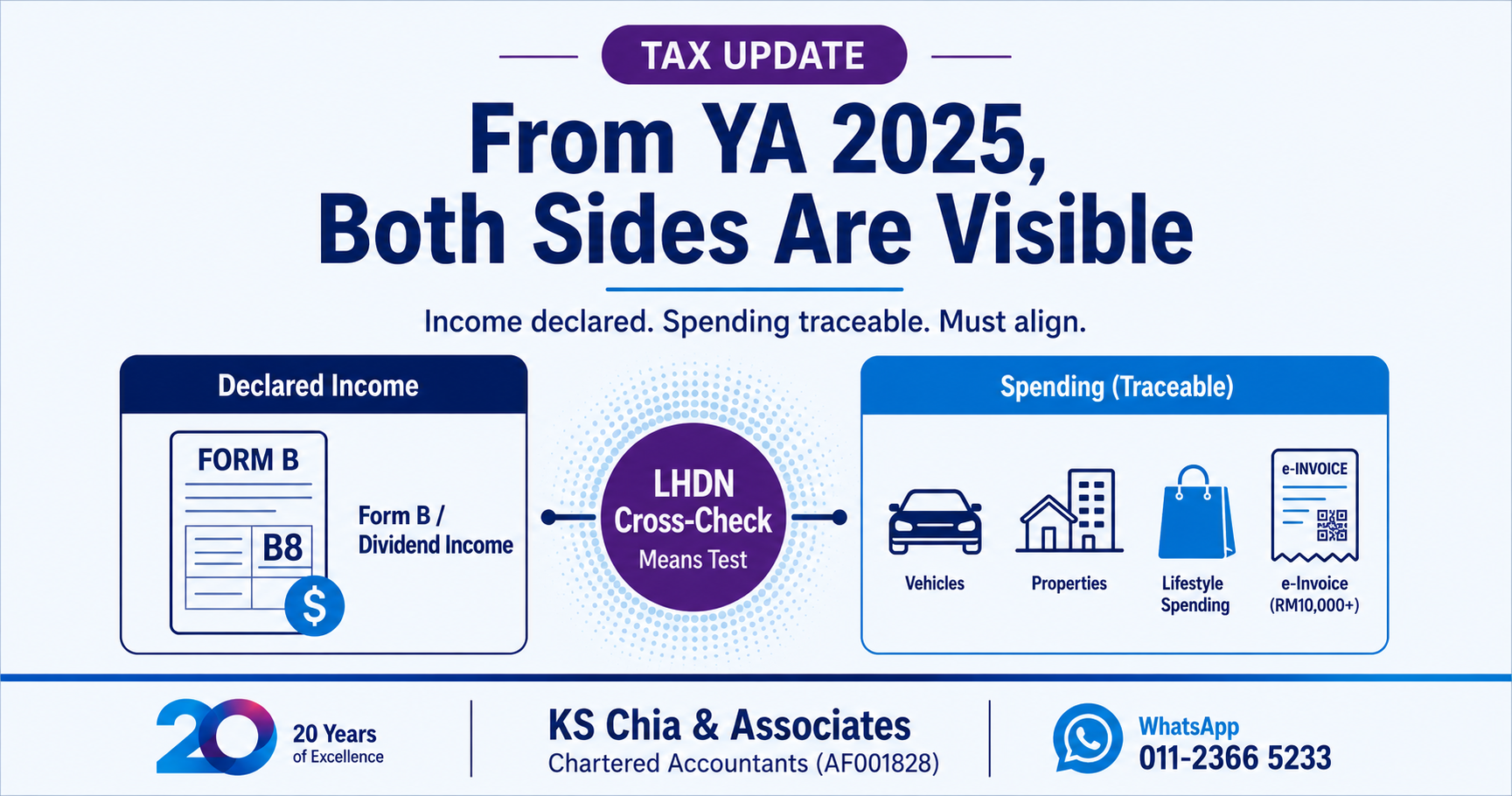

LHDN’s means test (ujian kemampuan) has always compared declared income against assets — properties, vehicles, company shareholdings. From the e-Invoice era, a third layer has been added: individual transactions above RM10,000, recorded in MyInvois and accessible to LHDN.

This is not a future risk. For Phase 1, 2, and 3 businesses, this data is live now.

What the RM10,000 Threshold Means

Every sale above RM10,000 by a Phase 1, 2, or 3 business requires an individual validated e-Invoice submitted to MyInvois. That record includes the buyer’s details, transaction date, amount, and nature of the supply.

For a company director making personal purchases from compliant businesses, the following are now individually documented:

- Luxury watches, jewellery, and handbags from compliant retailers

- High-end renovation works billed as a single invoice

- Premium hotel stays above RM10,000 per transaction

- Business-class air tickets above RM10,000 per booking

- Private medical or dental procedures above RM10,000

Phase 4 businesses (annual turnover up to RM5 million) are under a relaxation period until 31/12/2027 under e-Invoice Specific Guideline Version 4.7, Section 16.2(a). However, their purchases from Phase 1, 2, and 3 sellers are still recorded on the seller’s side.

Businesses with annual turnover below RM1 million are fully exempt from e-Invoice implementation.

Three Data Layers LHDN Now Has

| Layer | Source |

|---|---|

| Assets owned | JPJ, land registry, company records |

| Income declared | Form B, including dividend income from YA 2025 |

| Individual spending above RM10,000 | MyInvois — Phase 1/2/3 transactions |

A gap in any one of these three dimensions can trigger a means test assessment — at desk level, without a field visit.

Transaction Splitting Is Not a Solution

Deliberately splitting a single transaction to fall below the RM10,000 threshold is the type of anomaly LHDN’s data-matching analytics is designed to detect. Repeated near-threshold transactions from the same seller on adjacent dates will surface as a pattern. This creates an additional compliance risk, not a workaround.

What Director-Shareholders Should Do Now

- Review whether declared income — employment, rental, dividend, and other sources — is consistent with both asset accumulation and individual spending above RM10,000.

- If you are a Phase 4 business, note that your own e-Invoice obligations are under relaxation, but your spending from Phase 1/2/3 sellers is already recorded.

- If there is a gap between declared income and lifestyle, seek advice before LHDN assembles the picture independently.

This article is prepared for general information only and does not constitute professional advice tailored to your specific circumstances. Please consult a qualified tax adviser before taking action.

Not sure whether your tax position is consistent with your spending pattern? Contact KS Chia & Associates Chartered Accountants (AF001828) for a review.

WhatsApp us at 011-2366 5233