15 Jun 2% Dividend Tax for YA 2025: What Malaysian Business Owners and Investors Need to Know

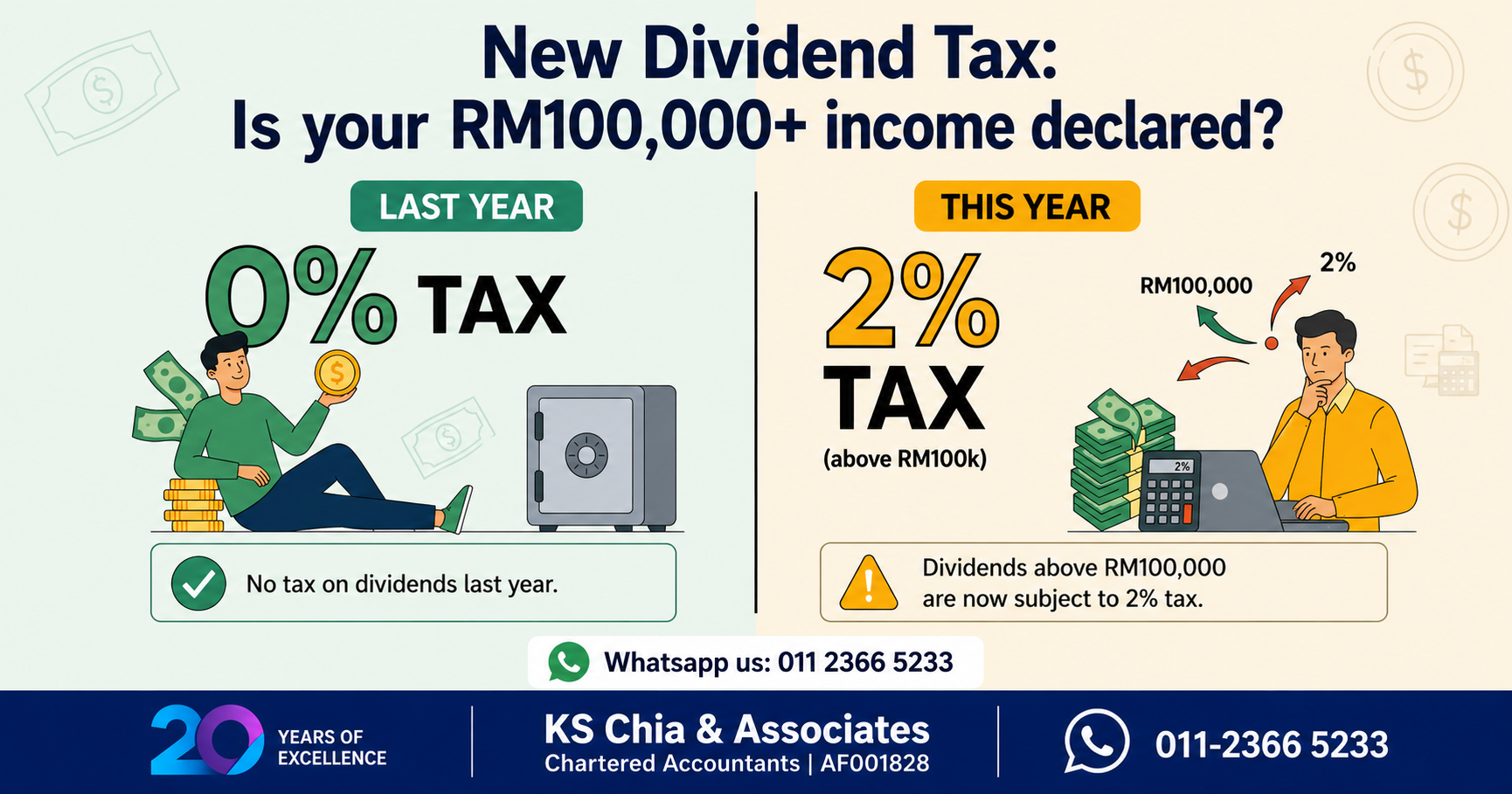

For years, Malaysian taxpayers have relied on a simple rule: under the single-tier system, dividends received from Malaysian companies are tax-free. Many business owners and investors have grown used to carrying forward the same treatment year after year when filing Form B. Starting from Year of Assessment (YA) 2025, that assumption needs to be revisited.

LHDN has introduced a new 2% Dividend Tax effective YA 2025. As the first year under this rule, incorrect declarations can lead to penalties under Section 112(3) or Section 113(1) of the Income Tax Act 1967 for submitting incorrect returns.

What Changed with Dividend Tax in Malaysia?

To broaden the tax base, the government now imposes a 2% tax on dividend income distributed by a company to individual taxpayers that exceeds RM100,000 per annum. This applies whether the dividend is received in cash or in-specie.

Key facts:

- The tax applies to dividends from both listed and unlisted shares in Malaysia.

- It affects resident individuals, non-resident individuals, and individuals holding shares through nominees.

- Only the portion of dividend income exceeding RM100,000 is subject to the 2% tax.

How the Tax Is Computed

Dividend income can no longer simply be combined with business or employment income in a single computation. Under the rules effective from YA 2025, dividend tax requires a separate computation using a statutory formula (A/B × C) under Part XXII of Schedule 1.

This means Form B now has a split structure:

- Part BA (Item B8): Statutory dividend income is reported here, separate from other income sources.

- Part BB (Item B26): Chargeable income subject to the dividend tax, calculated using the formula.

- Part BB (Item B27): The 2% tax applied to the B26 amount.

- Part BB (Item B28): Remaining chargeable income, taxed at normal scale rates.

KS Chia’s take: The B8 → B26 → B27 → B28 mapping is the part most likely to go wrong in the first filing cycle. An incorrect split between dividend and non-dividend income does not just misstate one line — it cascades through the rest of the form. This is worth a dedicated review before submission, not a quick check at the end.

Exemptions: Not All Dividends Are Affected

The following dividend sources remain exempt and fall outside the 2% tax:

- Profit distributions from the Employees Provident Fund (EPF / KWSP)

- Distributions from Amanah Saham Nasional Bumiputra (ASNB)

- Distributions from Lembaga Tabung Angkatan Tentera (LTAT) or unit trusts

- Overseas (foreign-source) dividend income

- Dividends from companies enjoying pioneer status or reinvestment allowances

- Dividends distributed by co-operatives

Who Needs to Be Careful?

The taxpayers most exposed to this change are:

Business owners and directors — those who regularly extract profits from their private companies (Sdn Bhd) via dividends instead of salaries.

High-net-worth investors — individuals holding significant portfolios of listed shares on Bursa Malaysia.

Joint assessment filers — spouses filing together must now separately disclose the dividend-earning spouse’s statutory dividend income.

KS Chia’s take: Director-shareholders who structure remuneration primarily through dividends should run a quick calculation now — if total dividend income for YA 2025 is approaching or exceeding RM100,000, the B26 computation is not optional arithmetic. It directly affects the final tax payable, and getting it wrong in the first year is the kind of error that draws LHDN’s attention precisely because so many taxpayers will be making the same mistake simultaneously.

Need Help Navigating YA 2025?

Do not assume your dividends are still fully tax-free. The first year of a new tax rule is when the most costly filing mistakes happen. Our team can review your dividend income position and handle the B8 / B26 / B27 / B28 computations as part of your Form B preparation.

Contact KS Chia & Associates Chartered Accountants (AF001828) for professional tax advisory and compliance services.

WhatsApp us at 011-2366 5233

This article is prepared for general information only and does not constitute professional advice tailored to your specific circumstances. Please consult a qualified tax adviser before taking action.